The landscape of public transportation in India is undergoing a structural pivot. While the shift toward electric buses (e-buses) began as an environmental initiative, the geopolitical crisis in West Asia hastransformed it into a matter of national energy security.

The current conflict involving Iran has significantly tightened the “oil-noose,” with Brent crude testing levels above $100-$120 per barrel and the closure of the Strait of Hormuz disrupting nearly 20% of global LNG trade. For India, this has translated into volatile pump prices and a 50-60% spike in LNG costs, making the traditional “clean” alternative—CNG—less economically viable than it was two years ago.

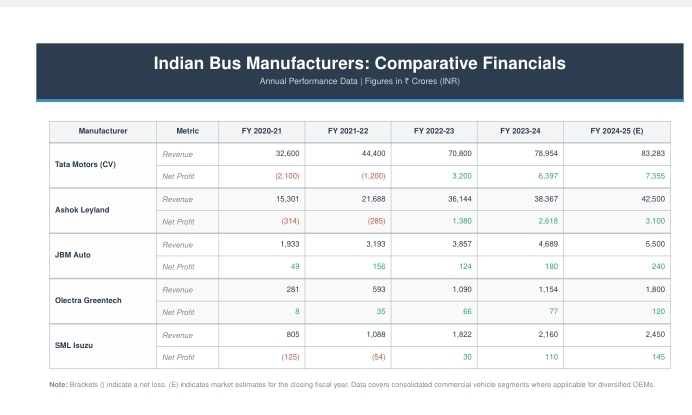

- Key Listed Players: The Manufacturing Powerhouses

The Indian e-bus market is currently dominated by a few key listed entities that have successfully transitioned from prototypes to mass production. - The Indian government has accelerated its targets to shield the economy from fossil fuel shocks:

- PM e-Bus Sewa: Aiming to deploy 10,000 air-conditioned e-buses across 169 cities. As of early 2026, tenders for over 6,000 buses are already concluded.

- PM E-DRIVE: Launched with an outlay of ₹10,900 crore, this scheme has replaced FAME-II, specifically incentivizing e-buses, e-trucks, and charging infrastructure through 2028.

- Payment Security Mechanism (PSM): A critical ₹3,435 crore fund that protects manufacturers against payment defaults by cash-strapped STUs, making the sector “bankable” for private investors.

- Net Zero 2070: The long-term goal is to have 40% of all new bus sales be electric by 2030, with a focus on 100% electrification of city bus fleets in major metros like Delhi and Bengaluru.

3. Impact of the Iran Conflict: The “Electric Push” Factor

The war in Iran has acted as a catalyst for three major shifts in the industry:

- CNG’s Fall from Grace: Previously, CNG was the bridge fuel. However, with the Strait of Hormuz disruptions, LNG import prices have skyrocketed. This has narrowed the price gap between running a CNG bus and an electric bus, making the latter more attractive.

- Energy Sovereignty: The government now views EVs not just as “green,” but as “secure.” Domestic solar and wind power are becoming the primary “fuel” for transport, bypassing the volatility of the Persian Gulf.

- Incentive Realignment: We are seeing a move toward Gross Cost Contract (GCC) models, where the government pays per kilometer. This allows cities to scale fleets without the massive upfront capital hit of high diesel prices.

4. How the Future Will Unfold

The next 24-36 months will likely follow this trajectory:

- Consolidation: Smaller players may struggle with the high R&D costs of battery thermal management, leading to the dominance of the “Big Four” (Tata, Ashok Leyland, JBM, Olectra).

- Battery Chemistry Pivot: Expect a faster transition toward LFP (Lithium Iron Phosphate) and emerging Sodium-ion technologies to reduce dependence on expensive imported minerals, further lowering costs.

- Inter-city Expansion: While current e-buses are mostly urban, the rollout of high-speed charging corridors will see 200km+ inter-city electric routes becoming standard.

- Grid Integration: Buses will transition from “consumers” to “storage.” Large e-bus depots will act as massive batteries (V2G – Vehicle to Grid) to stabilize the Indian grid during peak demand.

The Bottom Line: The combination of aggressive government subsidies and a global energy crisis has reached a “tipping point.” The e-bus industry is no longer an experiment; it is the frontline of India’s economic resilience.