India’s electric two-wheeler industry has evolved rapidly, shaped by two distinct pioneers: Ather Energy and Ola Electric. Their journeys reflect contrasting philosophies — one of steady, sustainable growth, and the other of explosive expansion followed by volatility.

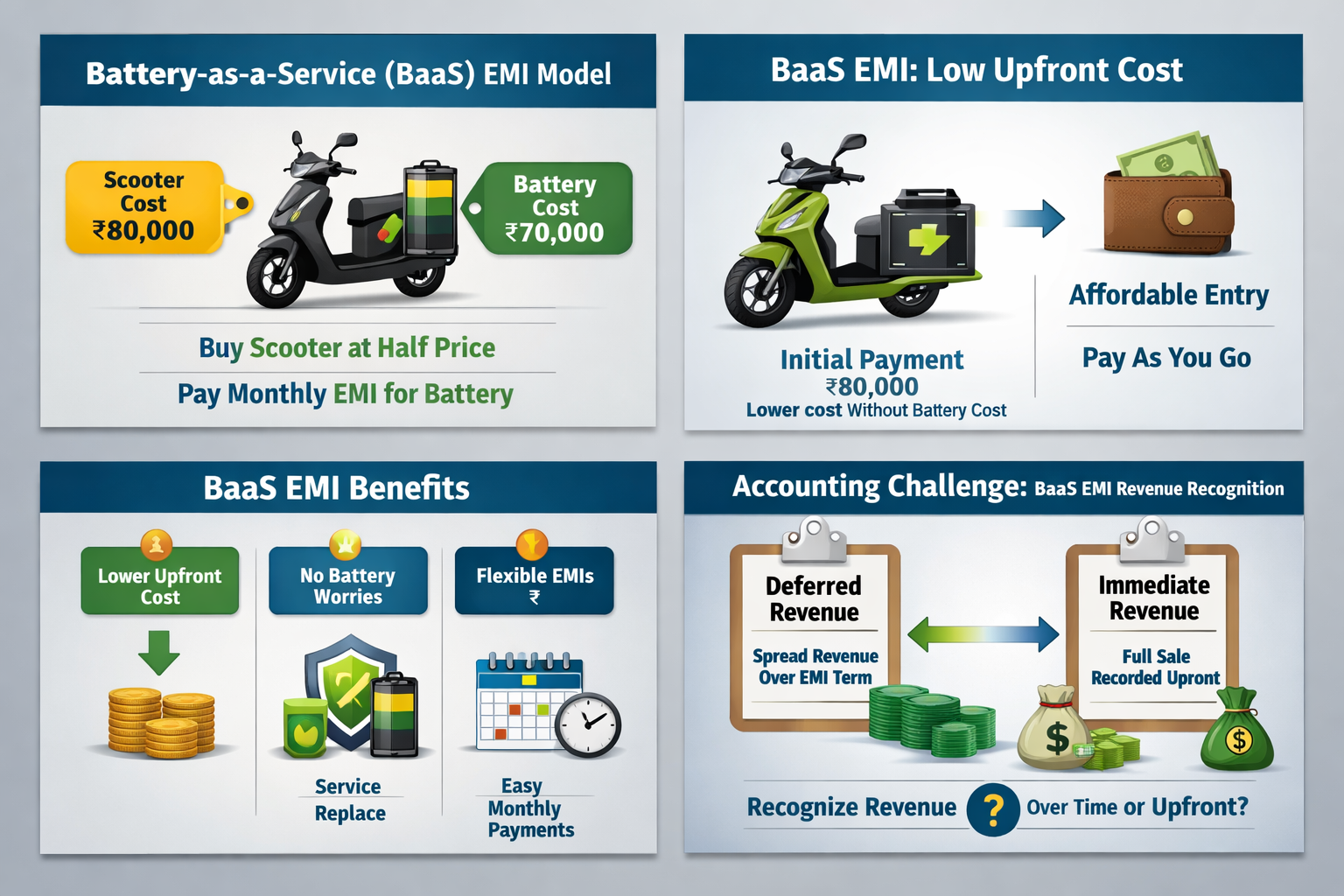

Ather’s growth is not just about sales volumes but also about financial innovation. Even today, Ather (alongside Hero) offers scooters under a Battery-as-a-Service (BaaS) model. In this scheme, scooters are sold at half price because the battery is excluded from the upfront cost. Instead, customers pay a BaaS-EMI — essentially a monthly installment for the battery.

This means the company is giving the battery away for free upfront, while monetizing it through recurring payments. This model lowers entry barriers, makes EVs more affordable, and ensures long-term customer engagement.

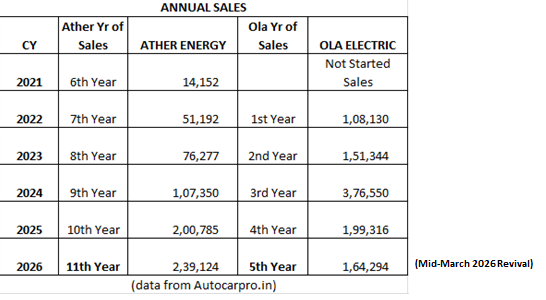

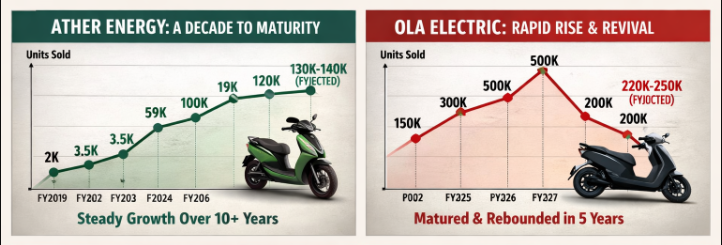

This trajectory shows that Ather took more than 10 years from incorporation to reach maturity in sales volumes. Its cautious approach — focusing on premium scooters, charging infrastructure, and city-by-city expansion — ensured resilience but required patience.

BaaS Accounting Complications:

BaaS model introduces accounting complications. Should the sale of the battery be recognized immediately in the current year, or should it be deferred and spread across the EMI term?

The answer has implications for revenue recognition, profit reporting, and investor perception. If recognized upfront, sales appear stronger but may misrepresent long-term liabilities. If deferred, financials reflect recurring income but dilute short-term performance. This tension highlights the complexity of EV financing innovation.

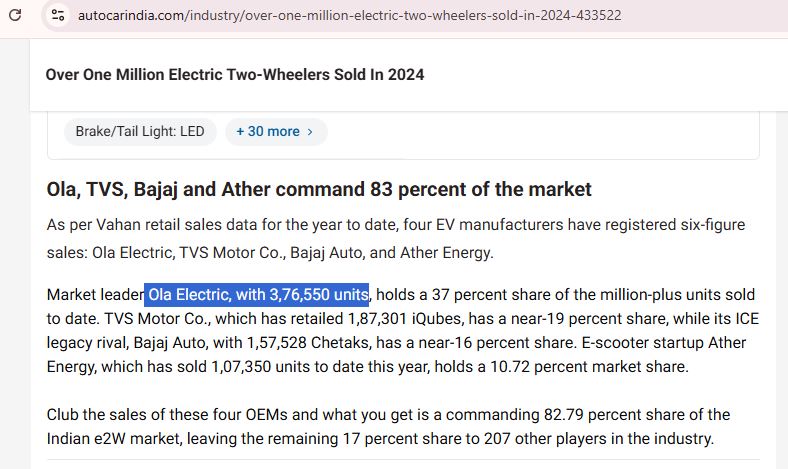

Ola Electric: Explosive Entry, Volatile Trajectory

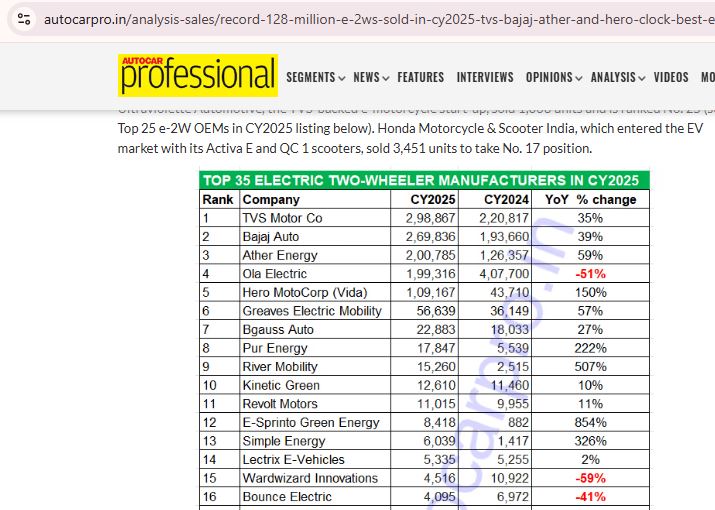

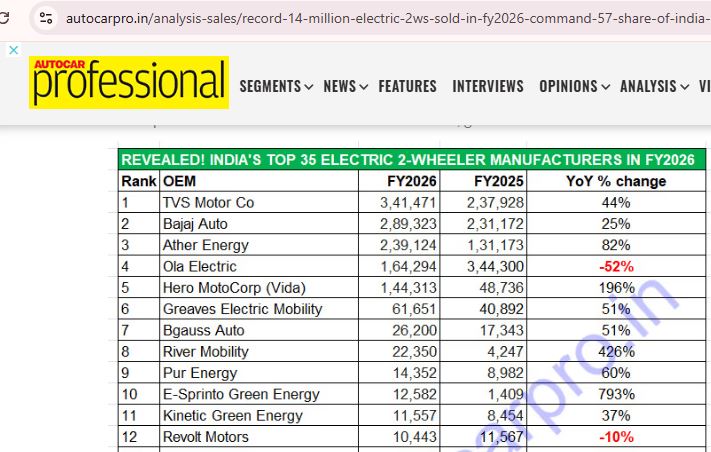

Ola Electric’s entry was dramatic. Its first full year of sales in FY2022 saw ~1.5 lakh units, rising to ~3 lakh in FY2023 and peaking at ~5 lakh in FY2024. However, subsidy cuts in FY2025 halved sales to ~2.5 lakh, and FY2026 saw further decline to ~2–2.2 lakh.

FY2027 projections suggest ~2.2–2.5 lakh units, driven by new models like RoadsterX bike and Shakti power backup system. FY 2027 could also be the year that Ola launches Z-Series scooter priced around Rs 60,000 and also expands into ContainerBESS.

Unlike Ather, Ola has not embraced BaaS financing. Its strategy has relied on aggressive pricing, subsidies, and mass-market scaling. While this captured market share quickly, it left Ola vulnerable to policy changes and profitability pressures.

Unlike Ather, Ola did not take a decade to mature. In fact, Ola achieved maturity and revived its sales trajectory within just 5 years of launch. Its aggressive pricing, direct-to-consumer model, and rapid scaling through the Futurefactory enabled it to dominate volumes quickly.

This left Ola vulnerable to subsidy cuts, but its ability to rebound within half a decade underscores its adaptability.

Lessons for India’s EV Market

- Sustainability vs Speed: Ather’s decade-long climb shows resilience, while Ola’s five-year maturity highlights aggressive adaptability.

- Policy Dependence: Subsidy cuts destabilized Ola, but Ather’s BaaS model cushioned affordability.

- Accounting Complexity: Innovative financing models like BaaS demand new approaches to revenue recognition.

- Consumer Trust: Ather and Hero’s financing innovation builds loyalty, while Ola’s mass-market approach faces volatility.

Conclusion

Together, Ather Energy and Ola Electric embody India’s EV revolution. Ather’s slow, steady climb and BaaS financing innovation reflect resilience and affordability, while Ola’s meteoric rise, sharp correction, and revival within five years illustrate the power of aggressive scaling.

As FY2027 unfolds, Ather and Hero’s BaaS-EMI model show that they are on a strong path… while Ola’s revived sales shows that Ola Energy has finally MATURED into the company it needs to be.

Year 2026… especially after Q1 results in August-2026… things could get very exciting for Ola Electric.