The Indian Electric Vehicle (EV) infrastructure ecosystem has hit a decisive fork in the road. For two-wheelers (E-2W) and three-wheelers (E-3W), the choice between a battery swapping network and a public charging station network is no longer a theoretical debate—it is a battle of operational unit economics, real estate footprint, and capital efficiency.

1. Battery Swapping: Rates & Market Realities (2026) Battery swapping fundamentally decouples the cost of the asset (the vehicle) from the energy source (the battery).

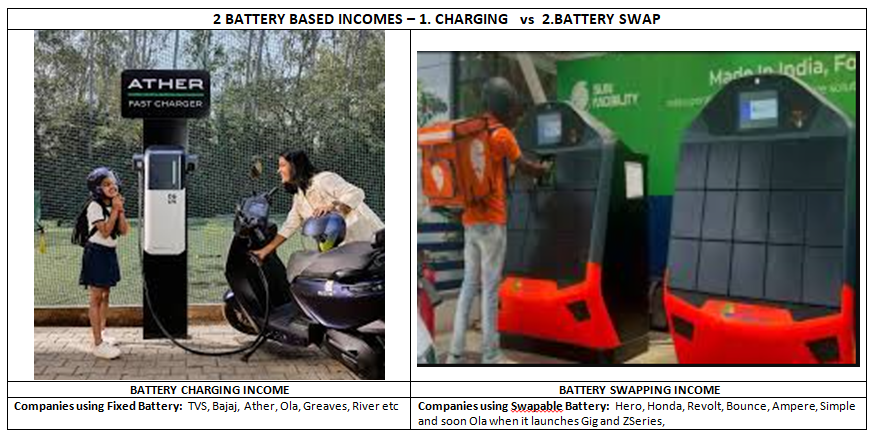

The most significant technical rift in the market today lies in battery architecture, which directly dictates the company’s long-term revenue potential.

Ather Energy (Fixed Asset Constraint): Ather remains committed to a fixed-battery design. While this allows for superior thermal management (using the chassis as a heat sink) and high performance, it limits the company’s flexibility.

In Ather’s Battery-as-a-Service (BaaS) model, the customer pays a lower upfront price, but the battery remains physically tied to the scooter.

This setup primarily benefits the financer (bank) rather than the manufacturer or the user; the rider often pays a monthly fee for a set “distance bracket” (e.g., 1,000 km), even if their actual usage is significantly lower (e.g., 700 km).

Ola Electric (The Swapping Pivot): In a strategic 2026 pivot, Ola has introduced removable, portable batteries in its Gig and S1 Z series. Unlike the fixed packs in the S1 Pro, these portable units allow Ola to tap into the high-frequency swapping ecosystem.

This hardware shift is a direct attack on the B2B segment, where downtime is expensive.