The Indian Electric Vehicle (EV) infrastructure ecosystem has hit a decisive fork in the road. For two-wheelers (E-2W) and three-wheelers (E-3W), the choice between a battery swapping network and a public charging station network is no longer a theoretical debate—it is a battle of operational unit economics, real estate footprint, and capital efficiency.

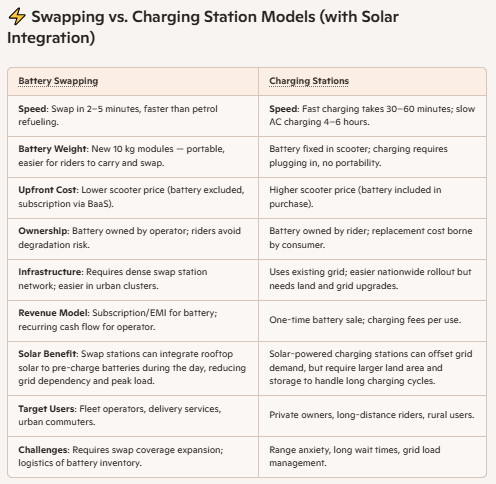

1. Battery Swapping: Rates & Market Realities (2026) Battery swapping fundamentally decouples the cost of the asset (the vehicle) from the energy source (the battery).

In India, this market is heavily dominated by commercial B2B fleets, delivery agents, and e-rickshaws where vehicle uptime directly equals income.

The TCO Comparison:

A delivery rider running 100 km daily spends roughly ₹9,500/month on a petrol scooter (fuel + maintenance). A swapping subscription drops that total operational cost to around ₹4,500/month—effectively cutting expenses by over 50%.

Revenue Generation: Driven by high-velocity recurring subscriptions and per-swap margins. A single 20-slot kiosk can service 10–12 swaps per hour because vehicle turnaround takes less than 2 minutes.

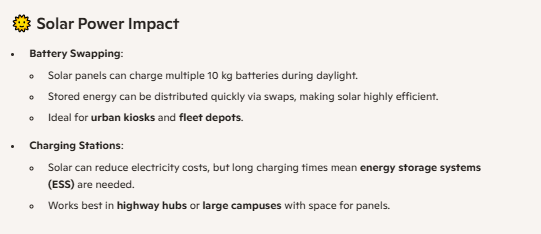

Profit Margins: Gross transaction margins at scale hover around 30% to 50%. Because charging occurs under controlled ambient parameters inside the kiosk, operators can stretch the battery’s lifecycle ($SoH$ – State of Health) much better than a consumer fast-charging at home.

The Catch: Profitability is completely tied to utilization rate.

If a BSS operator buys 100 spare batteries and they sit idle in the racks, the capital depreciation kills the business. It requires an anchored contract with a delivery fleet (e.g., Zomato, Zepto) to break even safely.

Public Charging Stations (PCS) – Revenue Generation:

Billed directly per unit of electricity consumed (e.g., ₹18 to ₹25 per kWh) plus a nominal parking/convenience fee.

Profit Margins: Net profit margins are tighter, sitting around 15% to 25%. A DC fast charger can only service 1 to 2 vehicles per hour per gun. If a vehicle stays plugged in past its charging window, it blocks the revenue stream.

The Catch: Real estate lease costs and demand charges from local electricity boards (DISCOMs) can completely wipe out profits if the station experiences low footfall during non-peak hours.

4. Does Ola Electric Have a Unique Strategic Advantage?> The Short Answer: Yes. Ola Electric possesses a highly integrated vertical stack that gives it an unparalleled cost and ecosystem advantage—but only if they execute their portable battery pivot smoothly.

1. Absolute Control Over Cell Costs (The 4680 Factor)The battery pack accounts for 35% to 40% of an EV’s bill of materials. By manufacturing its own 4680 Bharat Cells (NMC chemistry) via its Gigafactory, Ola bypasses third-party margins from Chinese cell suppliers. This allows Ola to price its vehicles aggressively lower or capture massive margins that rivals like Ather, TVS, or Bajaj cannot match, as they rely heavily on imported cells or assembled packs.

2. Multi-Vehicle Cross-Utilization (The Ultimate Battery Hedge) Ola is creating a modular ecosystem across a highly diverse portfolio:

- Passenger Vehicles: eScooters… eMotorcycles… eSmallCar

- Commercial Vehicles: GigScooters… ZSeries Scooters… eRickshaws…

- Non-Vehicles: Home UPS (Shakti)… Industrial Container-size Battery (MahaShakti)

3. Fighting the BaaS & Swapping Dilemma: Historically, Ola was fully committed to a fixed-battery, home/hypercharger model. However, their transition toward portable, swappable architectures in commercial-oriented form factors (like the Gig and Z-Series) allows them to play both sides of the coin.

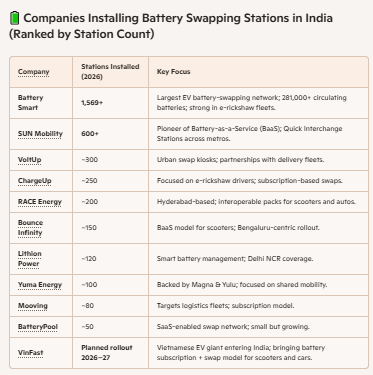

The Rival Constraint: Swapping networks like Battery Smart have to buy batteries from third parties and hope OEMs adopt their form factor.

The Ola SUPER Advantage: Ola can build its own swapping kiosks, populate them with its own low-cost proprietary cells, and seed the market with its own E-rickshaws and delivery fleets. They own the factory, the vehicle, the software, and the infrastructure.